CenterPoint Fund Accounting

- Setup & Processing of Tips

| Document #: | 3136 | Product: | CenterPoint Payroll |

|---|

Cash tips may be paid directly from a customer to an employee. Another way a tip may be paid is by the employee’s employer from a tip paid to the employee by the customer by way of credit card or check (an employer may choose to hold these types of tips and track the amounts in a Liability Account until the credit card or check payment has cleared). From a tax reporting point-of-view tips should be handled the same in both cases. Tips are not wages paid by an employer to an employee. The employer is only an intermediary in the exchange from the customer to the tipped employee. In CenterPoint, when tips are paid to the employee by the employer, they need to be paid as a non-taxable “Earning” (reimbursement). The tax reporting “Tips Earning” which is non-cash from the employer can be entered at the same time as a reimbursed tip (credit card receipt or check method) or at later date when the employee reports his tips. In CenterPoint that is also when taxes will be charged for tips. Therefore, wages or reimbursements should be included in the pay that will cover any taxes. Employee tips are normally included during payroll processing in order to properly calculate taxes. A tips earning will allow you to enter the employee's reported tips so taxes are calculated on the correct gross wages without increasing the employee's net pay.

Step A - Setup Tips Earning(s)

Step B - Assign Tips Earning to Employees

Step C - Enter Tips on a Pay Run

Step D - Tip Shortfall Allocation (optional - only if using Direct Tips)

Step A - Setup Tips Earning(s)

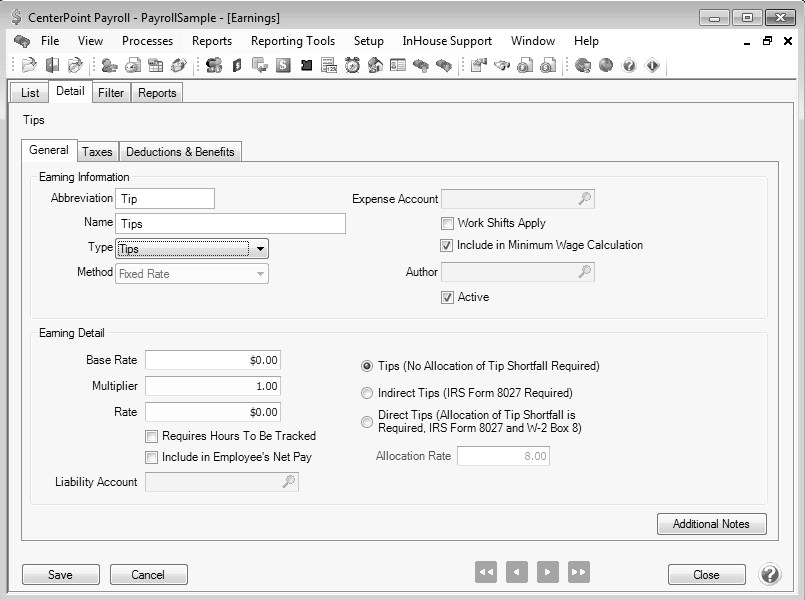

- Select Setup > Payroll Details > Earnings. Click New.

- Enter the Abbreviation and Name for this earning.

- Select Tips in the Type field.

- If you plan to hold employee tips until a credit card payment or check that generated the tip clears but want to include the tip amount in the net pay so taxes can be calculated, select the Include in Employee's Net Pay check box.

- If you selected the Include in Employee's Net Pay check box, select the Liability Account that you want to use to track the amount of the tips payable to your employee's so you can pay them on a future check.

- In the Earning Detail, specify the method to be used for this tips earning:

- Tips (No Allocation of tip Shortfall Required) - Usually used by small employers who are not required to allocate tips.

- Indirect Tips - Tips not received directly from a customer. For example, tips a busboy or dishwasher receives from a wait person. These tips do not appear in Box 8 of the W-2

- Direct Tips - Tips received directly from a customer, such as tips received by a wait person or bell person. These tips may be reported in Box 8 of the W-2.

- Tips (No Allocation of tip Shortfall Required) - Usually used by small employers who are not required to allocate tips.

- If you selected Direct Tips, enter the Allocation Rate. The standard allocation rate is 8% unless a lesser rate has been requested from the federal government.

- Select the Taxes tab. Specify the taxes that should and should not be calculated on these tips. For more information on how to use the Taxes tab, refer to the

- Click Save.

- If you have more than one type of tips, such as direct and indirect, repeat Steps 1 - 5 for each tip earning you will need.

Step B - Assign Tips Earning to Employees

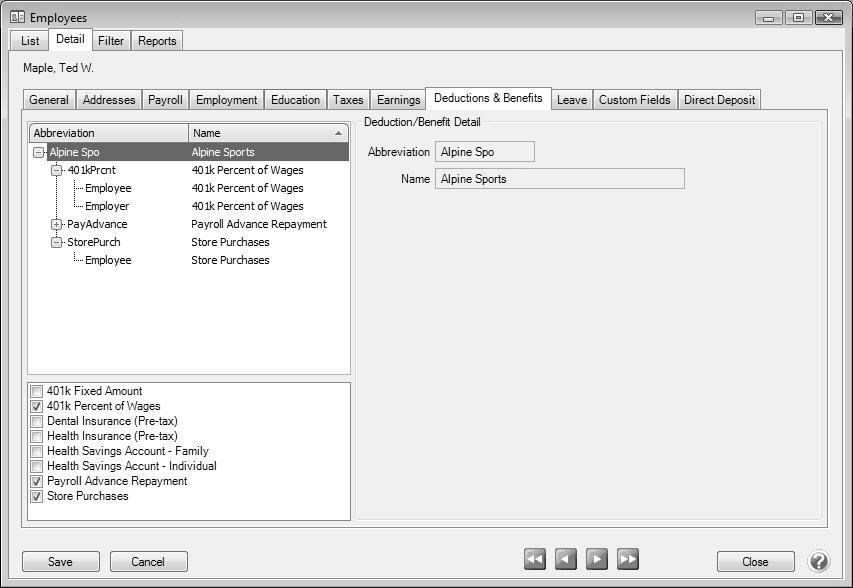

- Select Setup > Employees. Highlight the employee that will be receiving tips and click Edit.

- Select the Earnings tab.

- In the upper left, select the Employer. In the lower left-hand box check the box for the Tips earning. This will add the earning to the employee. It will automatically be displayed below the employer once it is selected in the lower left box.

- Click Save.

- Repeat Steps 1 - 5 for each employee who receives tips.

Step C - Enter Tips on a Pay Run

Processing a pay run with tips is the same as any other pay run. Please refer to the

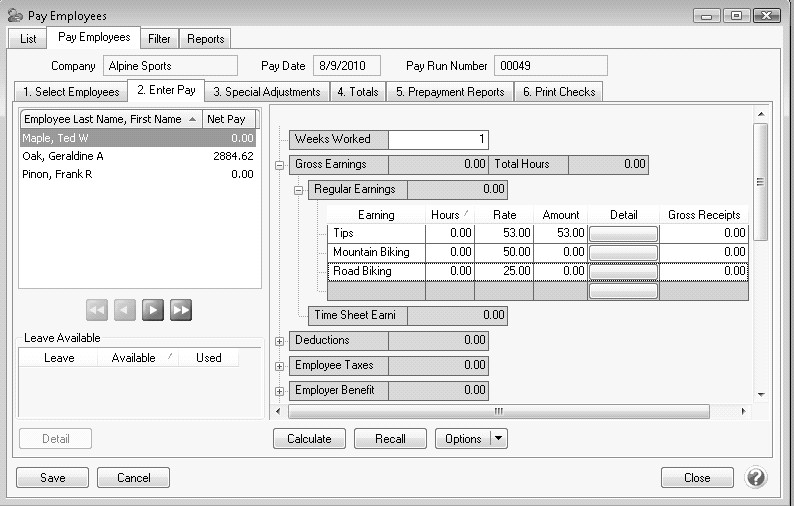

- Select Processes > Pay Employees or Processes > Payroll > Pay Employees and enter the pay run as usual.

- On the 2. Enter Pay tab, enter the employees' pay, including tips. Enter the total amount of tips reported in the Rate column for the Tips earning.

- If using Direct Tips, enter the employee's Gross Receipts for the pay period. To add Gross Receipts as a column, right click and select Add/Remove Columns. Check the box for Gross Receipts and click OK

- If you prefer, tips can also be entered using Time Sheets.

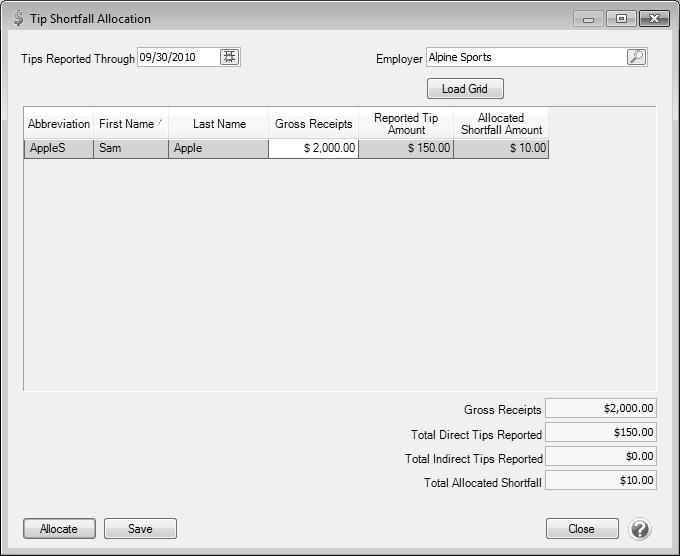

Step D - Tip Shortfall Allocation (Step D is only for those who selected "Direct Tips" as the method in Step A)

If you use direct tips, the Tip Shortfall Allocation is required. This will calculate a shortfall if the total reported tips are less than the total gross receipts multiplied by the allocation rate entered on the tips earning in

The standard shortfall rate is .08. No accounting transactions or tax calculations are posted when you use this selection.

- Select Processes > Tip Shortfall Allocation or Processes > Payroll > Tip Shortfall Allocation.

- Select a Tips Reported Through date. This defaults to the last day of the current month, but can be changed.

- Select your Employer.

- Click the Load Grid button.

- Review the information for each employee. If necessary, the Gross Receipts amount can be changed. The employee's reported tip amount cannot be changed on this screen.

- Click the Allocate button to calculate any shortfall amounts.

- The Total Direct Tips will display. This is the amount that will be used for the allocations.

- If you entered any earning codes for an employee pay run during the tips reported through date with an indirect tips method, the Total Indirect Tips will display. This amount is not used for the allocations.

- The Total Allocated Shortfall will display the total amount that was reported as tip shortfalls. Each employee will display an individual shortfall in the Allocated Shortfall Amount Column. This is the amount that will display in Box 8 on the employee W-2 forms and will add to the amount reported on the Employer IRS Form 8027.

- Click Save. You can then get a report of the calculated shortfalls by selecting Reports > Reports > Payroll Tax Data Reports > Tip Shortfall Allocation.

Examples of Paying Tips in CenterPoint

Below is a simplified example of a tip situation and two ways it could be handled in CenterPoint:

Sam Apple is a waiter the local diner, so he is a directly tipped employee. One evening he waited on two tables. The diner pays employees at the end of each week and includes tips reimbursed from credit cards and checks.

- The first customer paid him a $20.00 cash tip on a $50.00 receipt, which Sam stuck in his pocket.

- The second customer paid him a $5.00 tip on a$ 25.00 receipt and paid by credit card.

- At the end of the month, Sam reports to the employer that he made $6.00 in tips on $75.00 in gross receipts.

- In addition to tips, Sam was paid 24.00 in hourly taxable wages by the employer (8 hours * 3.00 per hour).

CenterPoint Example #1: Tip reporting only when the employee reports his tips.

The pay check received by Sam at the end of the week includes the following:

- Hourly Earnings: $24.00.

- Reimbursement: $5.00 (not taxable.)

- Federal Tax: No federal tax because the hourly earnings were not enough to have federal tax calculated.

- Social Security Tax: $1.49 (24.00 * .062).

- Medicare Tax: .35 (24.00 * .0145).

- Net Pay: $27.16

The pay at the end of the month when Sam reports his tips is as follows:

- Sam also gets paid for 3 hours that will cover the taxes for the tips reported.

- Hourly Earnings: $24.00.

- Tips Earning: $6.00 (this amount is not paid to employee. It is only for tax reporting purposes).

- Taxable Earnings: $30.00.

- Federal Tax: No federal tax because the hourly earnings were not enough to have federal tax calculated

- Social Security Tax: $1.86 (30.00 * .062)

- Medicare Tax: .44 (30.00 * .0145)

- Net Pay: $21.71

CenterPoint Example #2: Tip reporting at the time the employer pays the employee for credit card tips.

The pay check received by Sam at the end of the week includes the following:

- Hourly Earnings: $24.00.

- Tips Earning: %5.00 (this amount is not paid to employee, it is only for tax reporting purposes).

- Taxable Earnings: $29.00.

- Reimbursement: %5.00 (not taxable).

- Federal Tax : No federal tax because the hourly earnings were not enough to have federal tax calculated.

- Social Security Tax: $1.80 (29.00 * .062).

- Medicare Tax: .42 (29.00 * .0145)

- Net Pay: 26.78.

The pay at the end of the month when Sam reports his tips is as follows:

- Sam also gets paid for 3 hours that will cover the taxes for the tips reported.

- Hourly Earnings: $24.00.

- Tips Earning: $1.00 (this amount is not paid to the employee, it is only for tax reporting purposes).

- Taxable Earnings: $25.00.

- Federal Tax: No federal tax because the hourly earnings were not enough to have federal tax calculated.

- Social Security Tax: $1.55 (25.00 * .062).

- Medicare Tax: .36 (25.00 * .0145).

- Net Pay: $22.09.